A far-reaching new study suggests a staggering $21tn in assets has been lost to global tax havens. If taxed, that could have been enough to put parts of Africa back on its feet – and even solve the euro crisis

|

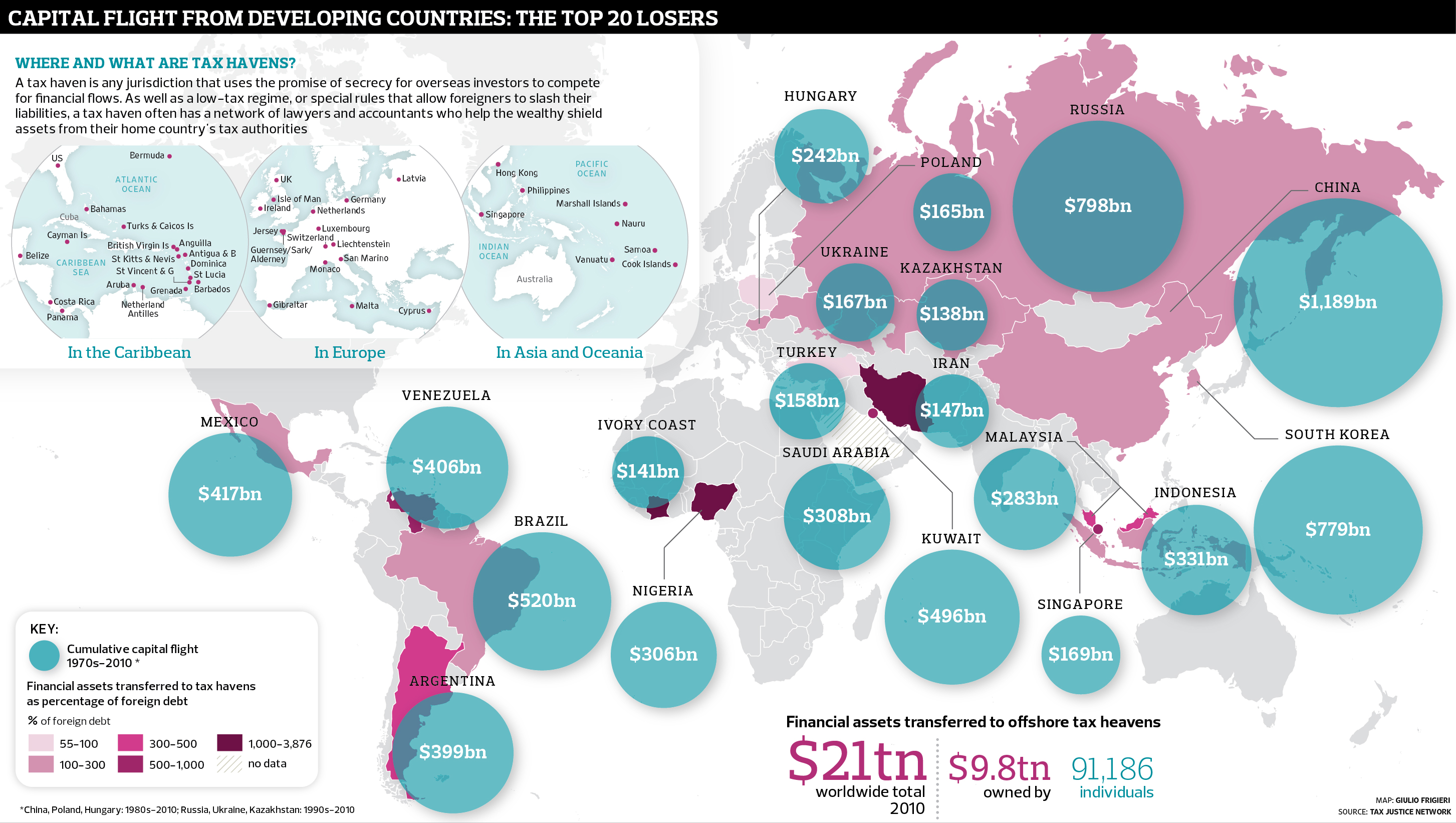

| Capital flight Illustration: Giulio Frigieri for the Observer (click here for a larger version of this graphic) |

{kind=link}

Heather Stewart

guardian.co.uk, Saturday 21 July 2012 16.00 EDT

Capital flight Illustration: Giulio Frigieri for the Observer (click here for a larger version of this graphic)

The world's super-rich have taken advantage of lax tax rules to siphon off at least $21 trillion, and possibly as much as $32tn, from their home countries and hide it abroad – a sum larger than the entire American economy.

James Henry, a former chief economist at consultancy McKinsey and an expert on tax havens, has conducted groundbreaking new research for the Tax Justice Network campaign group – sifting through data from the Bank for International Settlements (BIS), the International Monetary Fund (IMF) and private sector analysts to construct an alarming picture that shows capital flooding out of countries across the world and disappearing into the cracks in the financial system.

Comedian Jimmy Carr became the public face of tax-dodging in the UK earlier this year when it emerged that he had made use of a Cayman Islands-based trust to slash his income tax bill.

But the kind of scheme Carr took part in is the tip of the iceberg, according to Henry's report, entitled The Price of Offshore Revisited. Despite the professed determination of the G20 group of leading economies to tackle tax secrecy, investors in scores of countries – including the US and the UK – are still able to hide some or all of their assets from the taxman.

"This offshore economy is large enough to have a major impact on estimates of inequality of wealth and income; on estimates of national income and debt ratios; and – most importantly – to have very significant negative impacts on the domestic tax bases of 'source' countries," Henry says.

Using the BIS's measure of "offshore deposits" – cash held outside the depositor's home country – and scaling it up according to the proportion of their portfolio large investors usually hold in cash, he estimates that between $21tn (£13tn) and $32tn (£20tn) in financial assets has been hidden from the world's tax authorities.

"These estimates reveal a staggering failure," says John Christensen of the Tax Justice Network. "Inequality is much, much worse than official statistics show, but politicians are still relying on trickle-down to transfer wealth to poorer people.

"This new data shows the exact opposite has happened: for three decades extraordinary wealth has been cascading into the offshore accounts of a tiny number of super-rich."

In total, 10 million individuals around the world hold assets offshore, according to Henry's analysis; but almost half of the minimum estimate of $21tn – $9.8tn – is owned by just 92,000 people. And that does not include the non-financial assets – art, yachts, mansions in Kensington – that many of the world's movers and shakers like to use as homes for their immense riches.

"If we could figure out how to tax all this offshore wealth without killing the proverbial golden goose, or at least entice its owners to reinvest it back home, this sector of the global underground is easily large enough to make a significant contribution to tax justice, investment and paying the costs of global problems like climate change," Henry says.

He corroborates his findings by using national accounts to assemble estimates of the cumulative capital flight from more than 130 low- to middle-income countries over almost 40 years, and the returns their wealthy owners are likely to have made from them.

In many cases, , the total worth of these assets far exceeds the value of the overseas debts of the countries they came from.

The struggles of the authorities in Egypt to recover the vast sums hidden abroad by Hosni Mubarak, his family and other cronies during his many years in power have provided a striking recent example of the fact that kleptocratic rulers can use their time to amass immense fortunes while many of their citizens are trapped in poverty.

The world's poorest countries, particularly in sub-Saharan Africa, have fought long and hard in recent years to receive debt forgiveness from the international community; but this research suggests that in many cases, if they had been able to draw their richest citizens into the tax net, they could have avoided being dragged into indebtedness in the first place. Oil-rich Nigeria has seen more than $300bn spirited away since 1970, for example, while Ivory Coast has lost $141bn.

Assuming that super-rich investors earn a relatively modest 3% a year on their $21tn, taxing that vast wall of money at 30% would generate a very useful $189bn a year – more than rich economies spend on aid to the rest of the world.

The sheer scale of the hidden assets held by the super-rich also suggests that standard measures of inequality, which tend to rely on surveys of household income or wealth in individual countries, radically underestimate the true gap between rich and poor.

Milorad Kovacevic, chief statistician of the UN Development Programme's Human Development Report, says both the very wealthy and the very poor tend to be excluded from mainstream calculations of inequality.

"People that are in charge of measuring inequality based on survey data know that the both ends of the distribution are underrepresented – or, even better, misrepresented," he says.

"There is rarely a household from the top 1% earners that participates in the survey. On the other side, the poor people either don't have addresses to be selected into the sample, or when selected they misquote their earnings – usually biasing them upwards."

Inequality is widely seen as having increased sharply in many developed countries over the past decade or more – as described in a recent paper from the IMF, which showed marked increases in the so-called Gini coefficient, which economists use to measure how evenly income is shared across societies.

Globalisation has exposed low-skilled workers to competition from cheap economies such as China, while the surging profitability of the financial services industry – and the spread of the big bonus culture before the credit crunch – led to what economists have called a "racing away" at the top of the income scale.

However, Henry's research suggests that this acknowledged jump in inequality is a dramatic underestimate. Stewart Lansley, author of the recent book The Cost of Inequality, says: "There is absolutely no doubt at all that the statistics on income and wealth at the top understate the problem."

The surveys that are used to compile the Gini coefficient "simply don't touch the super-rich," he says. "You don't pick up the multimillionaires and billionaires, and even if you do, you can't pick it up properly."

In fact, some experts believe the amount of assets being held offshore is so large that accounting for it fully would radically alter the balance of financial power between countries. The French economist Thomas Piketty, an expert on inequality who helps compile the World Top Incomes Database, says research by his colleagues has shown that "the wealth held in tax havens is probably sufficiently substantial to turn Europe into a very large net creditor with respect to the rest of the world."

In other words, even a solution to the eurozone's seemingly endless sovereign debt crisis might be within reach – if only Europe's governments could get a grip on the wallets of their own wealthiest citizens.

• This article was amended on 23 July. In the original graphic Poland was shown in the wrong place. This has been corrected

0 nhận xét:

Đăng nhận xét